{kind=link}

Managing the availability and cost of raw materials remains a top priority for resource-dependent firms. A carefully planned and professionally implemented fibre strategy is an essential element for pulp and paper companies aiming at creating and sustaining competitive advantage.

Timo Suhonen, Pöyry Management Consulting

Fibre remains the major competitive differentiator between winners and losers in the global pulp and paper industry. Winners will regularly be those companies that can intelligently integrate low cost fibre sources with a high growth market. For some companies, big or small, upstream or downstream, the evolving fibre market has brought about new opportunities, whilst others have failed to capture these opportunities. The pivotal role of fibre raw materials means that developing a wall-to-wall fibre strategy to manage their costs and secure their availability should be a priority in the pulp and paper industry.

The global fibre market is not getting any easier. Regional supply/demand imbalances in the global fibre market will continue, and balancing these deficits will be an increasingly important challenge for the industry. Therefore, understanding forest and fibre supply dynamics and anticipating market changes are of strategic importance for all business participants.

Profound changes

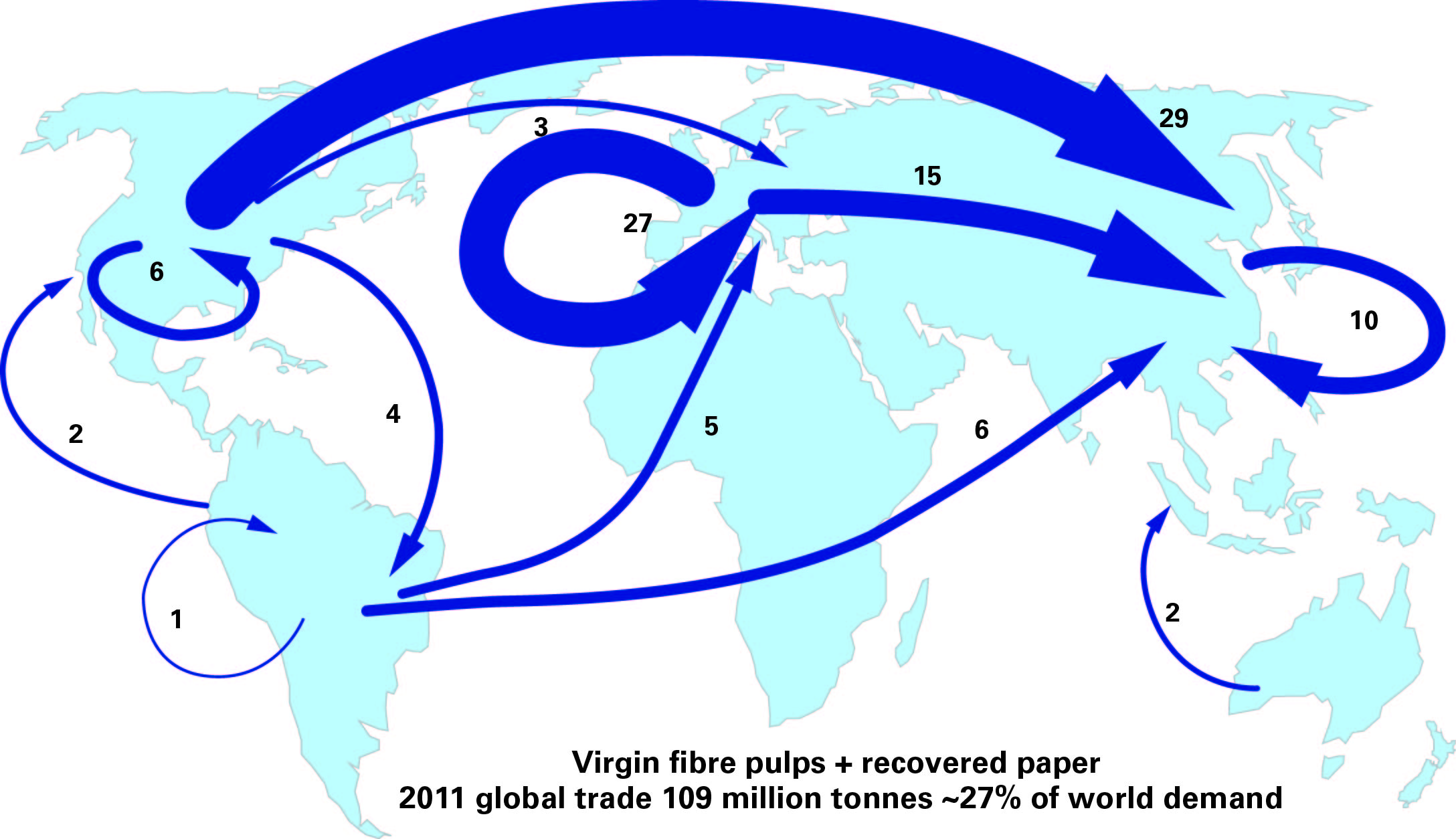

The global papermaking fibre markets have undergone gradual structural changes that continue to shape the pulp and paper industry. The strong contrast between the growth in the mature and emerging markets on one hand, and the uneven global distribution of fibre resources on the other, has been the key challenge of the pulp and paper industry as it seeks long-term success in the international and domestic markets. The uneven geographic distribution of fibre resources has boosted international papermaking fibre trade, which reached 109 million tonnes in 2011, corresponding to 27% of global consumption.

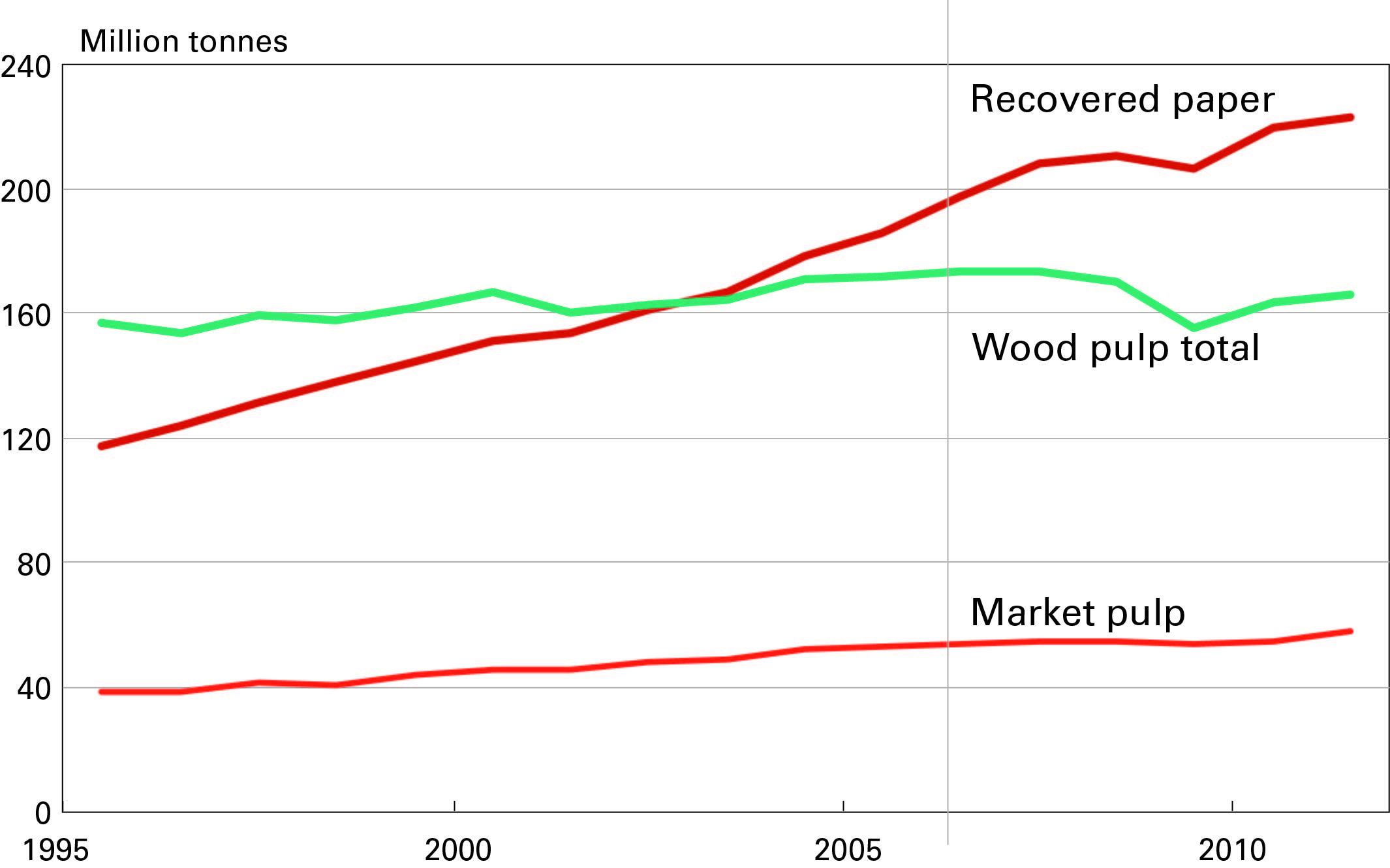

Despite economic challenges in the West, coupled with a continuous weakening demand for graphic papers in mature markets, the global consumption of papermaking fibre reached the all-time high of 407 million tonnes in 2011. Recovered paper consumption peaked at 223 million tonnes in 2011, while wood pulp totalled 166 million tonnes. The role of non-wood raw materials remained marginal from global standpoint, levelling at 17 million tonnes in 2011.

Medium-term fibre demand prospects are still very much uncertain, expected to be modest (at best) for mature markets, but much better for emerging regions of Asia and Latin America. However, the world economy is still fragile, and risks to the downside remain.

In the longer term, paper markets will grow slower than the world economy in general. Global economic growth is projected at 3.6%/annum through 2025, whilst paper and paperboard demand growth during the same period is estimated to be lower at 1.6%/annum. The main reason for income inelastic demand is the increasing availability of affordable substitutes for paper in advertising and communication-related end uses, and also in certain fibre-based packaging applications. Furthermore, declining basis weights and a tendency for light-weighting in packaging also play a role in this.

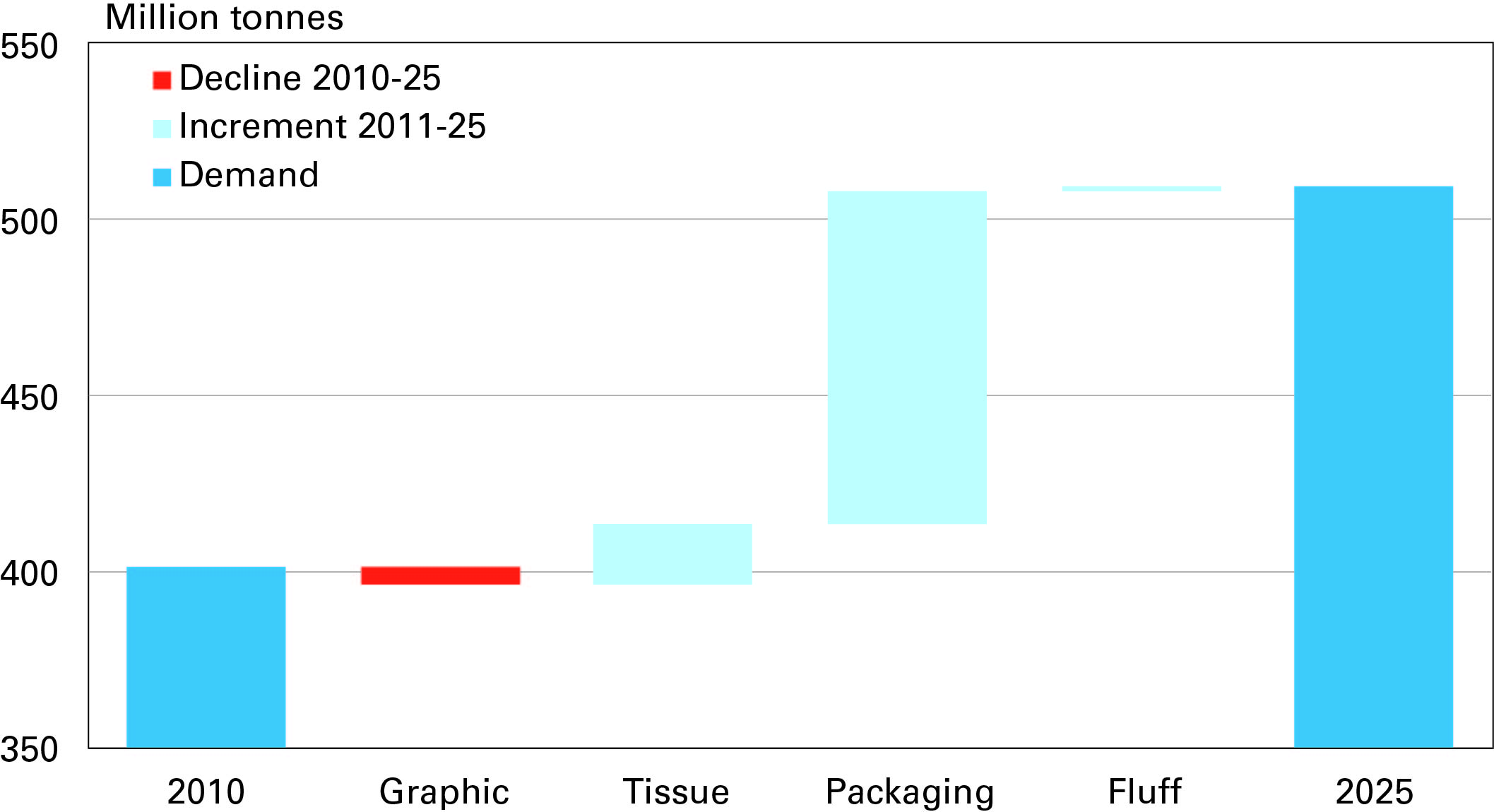

In line with the overall paper and paperboard demand, the world consumption of papermaking fibre and fluff pulps is expected to grow from the current 407 million tonnes to 510 million tonnes by 2025. The packaging board industry is the main growth driver globally, accounting for a good 85% of the projected incremental fibre demand through 2025. The tissue paper sector is another significant driver of fibre demand (~15% of projected incremental demand). Demand for fibre in the graphic paper sector is expected to decline.

The rising cost of recovered paper

Global recovered paper trade flows continue to surge. During the last decade or two, there has been a concerted strive to increase paper and paperboard collection and recycling in North America, Western Europe and Japan. As the fast-growing Asia races to catch up with the more mature economies, the supply of recovered paper is getting more strained.

With collection of recovered paper approaching its collectable potential in the West and Japan, the supply becomes increasingly inelastic. Marginal cost curve turns upward, and at some point becomes nearly vertical. In consequence, the global paper sector is now confronted with both increasing and highly volatile real prices of recovered paper raw material.

Furthermore, the potential for recovered paper as a source of energy will also drive up the costs of secondary fibre and thus aggravate the position of cost-conscious papermakers as possibilities to pass on incremental production costs to end users are evermore challenged. Under these circumstances, the pulp and paper sector should prepare itself for a future where recovered paper prices remain permanently at higher levels due to tightness of supply. Papermakers should therefore consider the opportunities for upstream integration and fibre strategies acquiring further and tighter control of recovered fibre flows.

The development of domestic recovered paper supply will be one of the fundamental competitive issues for the Asian paper industry into the future. High collection rates coupled with the stagnant or even declining paper demand in the West and Japan will eventually limit the growth of imported recovered paper in China and the rest of emerging Asia. Nevertheless, recovered paper will continue to be the primary source of fibre for the Asian paper and packaging board industry. Some Chinese companies – Nine Dragons, Lee & Man and Long Chen in the forefront – have strengthened their competitive position through establishing upstream recovered paper procurement operations in the West.

Graphic paper sunset

The emergence of new media will have important implications on papermaking fibre demand, including virgin pulps and recovered paper. The global newsprint industry is in secular decline, and consequently, the industry’s fibre requirements are forecast to decrease in the long term. Printing/writing paper production is declining in the West and Japan with a similar effect, and approaching maturity in the emerging markets, too.

Declining graphic paper consumption in mature markets inevitably leads to declining fibre consumption in the western industry. At the same time, it will limit the availability of recovered paper for collection, and cause fibre supply problems especially for the resource-poor regions such as Asia.

Yet, the production of tissue paper and packaging boards will continue to grow in the long term, driven in particular by the fast-growing Asian markets. For Asian paper and paperboard industry, the increasing complications in terms of offshore recovered paper supply, with particular reference to pre- and post-consumer graphic papers in the West, would probably mean a major stimulus for increased domestic collection, but also increasing recovered paper procurement costs and prices, and potential substitution of recovered paper by virgin fibre pulps.

Implications on market pulp business

The graphic paper sunset in the West will potentially lead to furnish changes in tissue, printing paper and boxboard production. The tissue paper industry will be on the front line as the true cost of high grade printing materials becomes less attractive for the tissue industry as compared to virgin fibre pulps. The price of recovered paper coupled with the process losses of high quality deinking grades (up to 35-40%), increased energy costs, and increasing landfilling costs for deinking sludge have deteriorated the competitiveness of secondary fibre in tissue paper production. It is for these reasons that the tissue industry has become an increasingly significant client segment for market pulp (BSKP and BHKP) producers, and especially for those using plantation-grown eucalypt raw materials.

The future of non-wood pulp is another important moving part impacting the future of the market pulp business globally. Tightening environmental regulations have already marginalized the role of straw, reed ecc. pulps in China. The country’s non-wood pulp mills are typically small with a history of inadequate environmental control facilities. Consequently, China’s non-wood pulp capacity is declining, despite the fact that new non-wood pulp mills are continuously being built. The evolving fibre gap will be filled partly by recovered paper, and partly by virgin fibre pulps, including market pulp.

New fibre baskets

Fostering upstream investments in traditional supply areas is an important alternative for paper companies trying to secure their fibre supply in the long term. But this comes with a price: land and labour costs are increasing faster than inflation, pushing up wood costs in Brazil, Uruguay and China, for example. This is triggering a search for alternative fibre baskets and innovation in forestry practices.

Will Africa be the next Eldorado for the pulp and paper industry? What about Indochina, PNG/Irian Jaya, Paraguay, etc. providing similar opportunities?

In fast-growing plantations, even those using modern technologies, labour costs can account for up to 40-60% of the delivered wood costs. Labour costs rising faster than overall inflation leads to increased mechanization and automation of forestry activities. The search for lower wood costs also triggers the adoption of enhanced bio-technologies with the promise of improved yield/input ratios.

The strategic choice

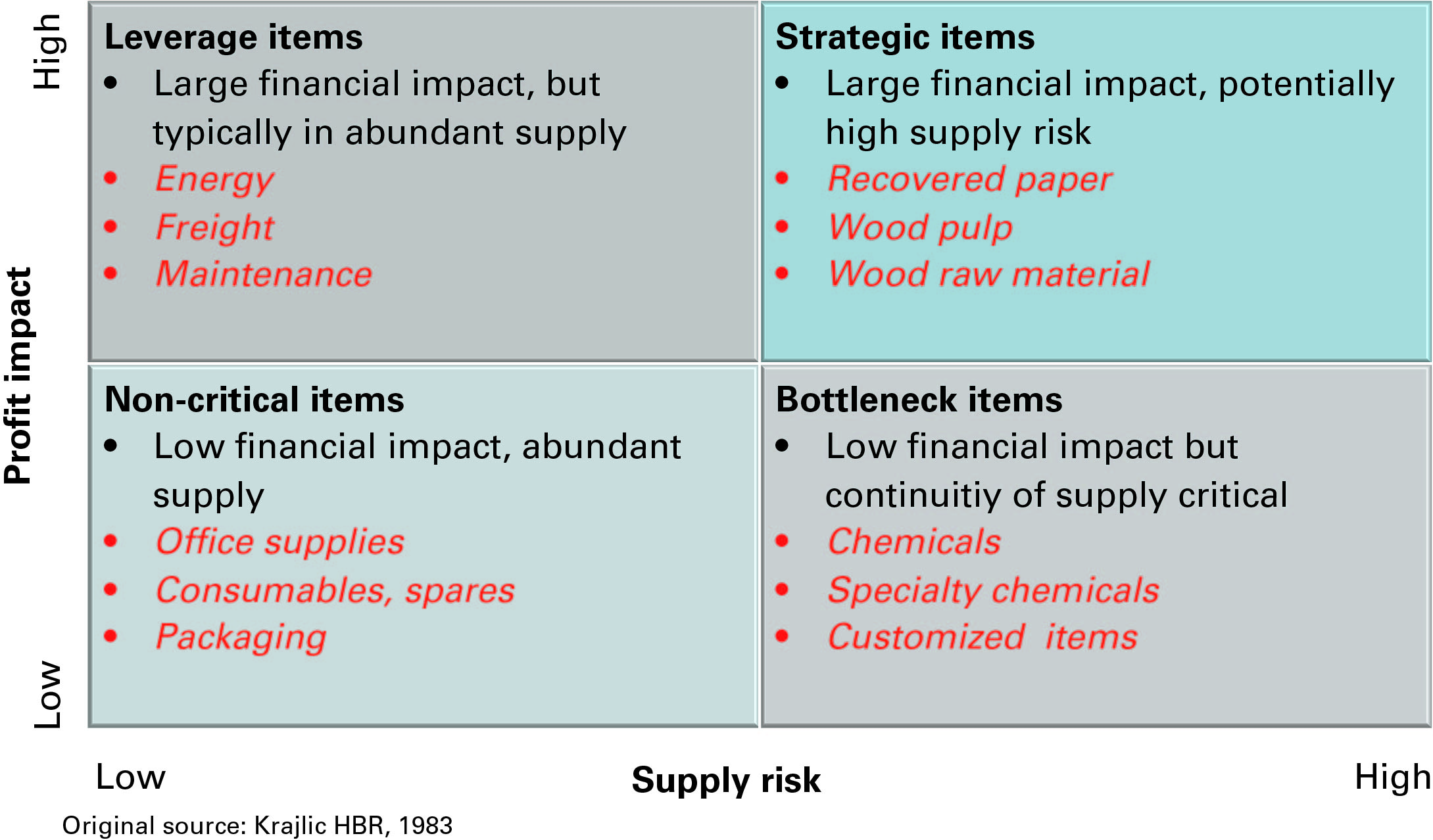

Upstream operations dealing with pulpwood, pulp and recovered paper supply are highly strategic featuring potentially high impact on profitability, but also high supply risk. It is clear that the leverage of procurement spend in fibrous raw materials is very high in terms of EBIT, and thus critical for the mature industry such as pulp and paper.

Acknowledging the risk of recovered paper shortages and price pressures globally, it is quite likely that more virgin raw materials, including fibre from fast-growing wood plantations will be needed. As consumers are becoming increasingly aware of issues of sustainability, also corporate upstream operations are getting tuned up towards holistic, multi-dimensional modus operandi seeking balance between economic, social and environmental goals.

Pöyry has an extensive track record over the decades on assignments that have helped resource-dependent firms in undertaking fibre strategy development across the globe and across a broad front of fibrous raw materials. The scope has varied, covering a range of raw materials, including indigenous or plantation wood, non-wood raw materials, market pulps, recovered paper and biofuel feedstock, to mention but a few.

I’d like to look more into the projections of demands such as, ” the world consumption of papermaking fibre and fluff pulps is expected to grow from the current 407 million tonnes to 510 million tonnes by 2025.”

Wondering where the citations are for the sources this article used? I need to find a credible source for a project that I’m working on about the paper industry.

Thanks!

Michelle

Comments are closed.