by Outi Juntti, Senior Principal, Pöyry Management Consulting Oy

Value of the global packaging market is estimated at over 800 billion USD i.e. at the same level than GDP of the Netherlands. The market is forecast to grow around 3 per cent per annum. Rapidly expanding markets in emerging regions especially China, India and South Eastern Asian countries as well Latin America are driving the growth. Asian packaging market is already larger than that of Europe or North America. However, steady growth is expected in the more mature economies as well.

Macroeconomic indicators like GDP, industrial production and consumer spending naturally form the foundation for the growth, but there are several other factors boosting demand including retail development and globalization, e-commerce, life-style changes like eating on-the-go; the list is endless. Food and beverages make over 40 per cent of the global packaging market value and when adding the other consumer products the share of consumer related packaging rises up to approximately 65 percent and industrial applications represent only 35 per cent of the business value. Thus the global packaging market is predominantly following and depending on the consumer behaviour and preferences. Furthermore there is a great breadth and variety of end-uses, regional differences and applications.

For these reasons the drivers and trends in the global packaging markets are complicated and not a single, universal factor can be nominated. However, some megatrends seem to be prevailing and impacting packaging business in most the markets globally.

There is a clear polarization of the consumers into the ones who are cost aware and the ones to whom other attributes like quality, prestige play a bigger role. Furthermore more and more regulations are influencing packaging formats and materials driven particularly by consumer safety and traceability requirements as well as environmental concerns. Therefore recyclability and reduction of packaging material resulting in light-weighting have become increasingly critical in nearly all geographies and end-uses.

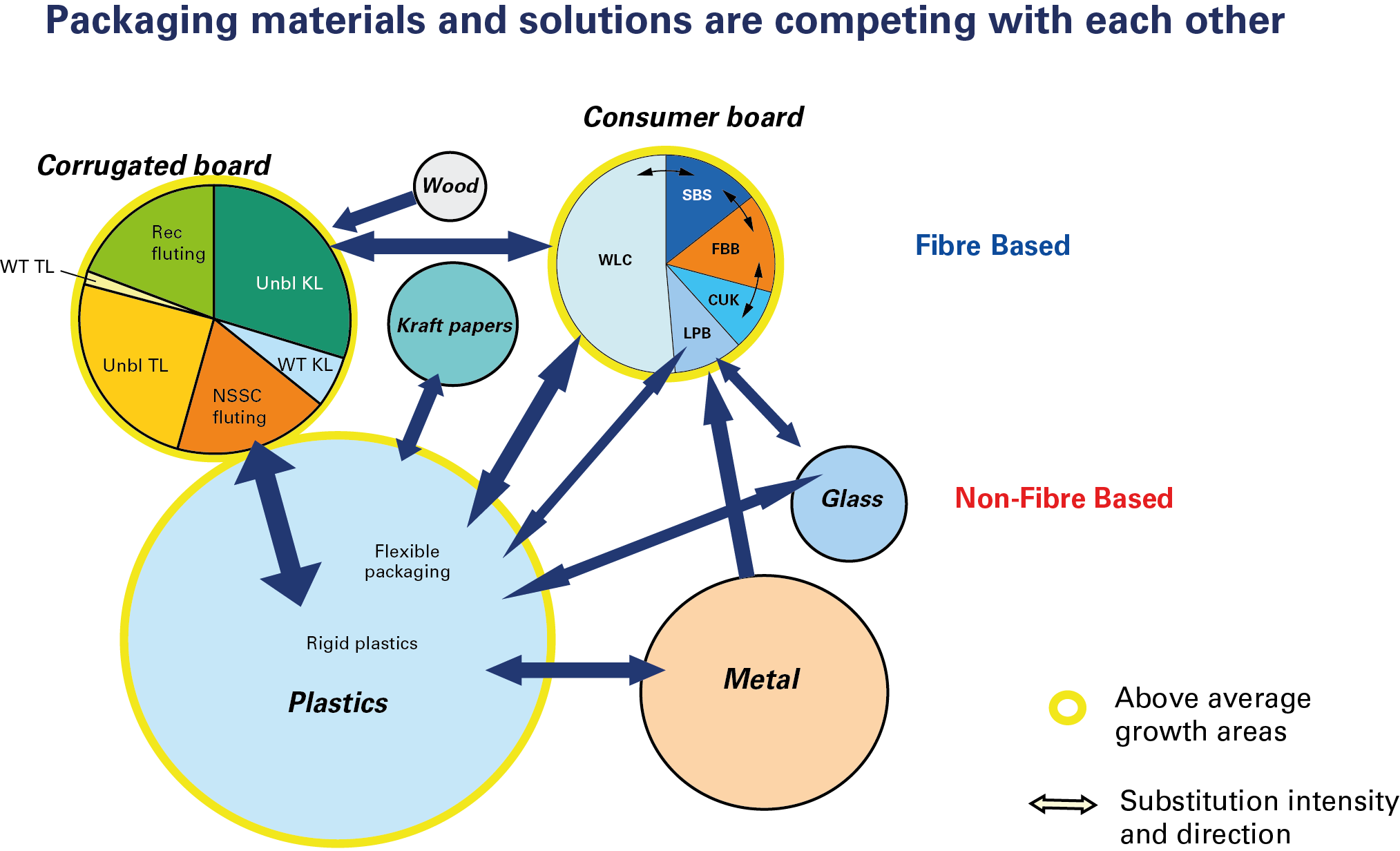

Different packaging materials and solutions are competing with each other

Fibre based solutions, cartonboards, packaging papers and corrugated board are doing nicely in this competition especially in the high-end products and transport packaging. By value fibre based packaging is the largest material, but by volume or number of packages plastics is the largest. Thus flexible and rigid plastic packaging is the main competing material for corrugated containers, folding cartons and packaging papers whilst metal and glass have been losing their share. However, substitution takes place into both directions and eg. cereals and biscuits are being packed into both folding cartons as well as on flexible packaging. Brand owners have a great impact on this as they make the strategic decision on the packaging solution depending on which segment, consumers or geographies they are targeting at with their products (figure 1, here under).

All in all, the global packaging industry is expected to continue demonstrating robust growth for fibre based solutions despite the potential for end-use substitution by non-fibre materials.

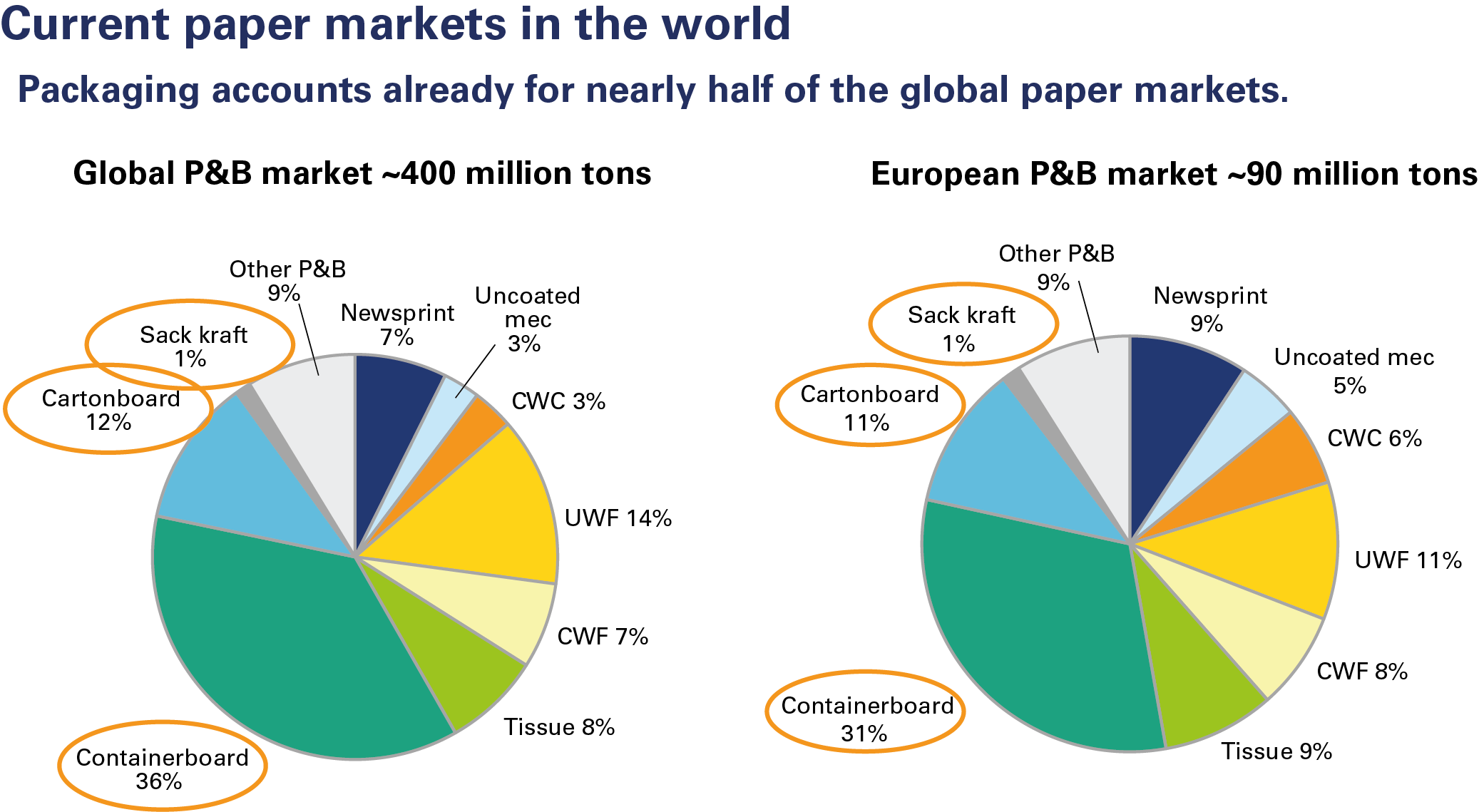

Containerboard is one of the fastest expanding segments of the global paper industry and it accounts already for nearly 40 per cent of the global paper and board market and over 30 per cent that of Europe. When combined with cartonboards and sack kraft packaging is already half of the global paper and board market (figure 2, under).

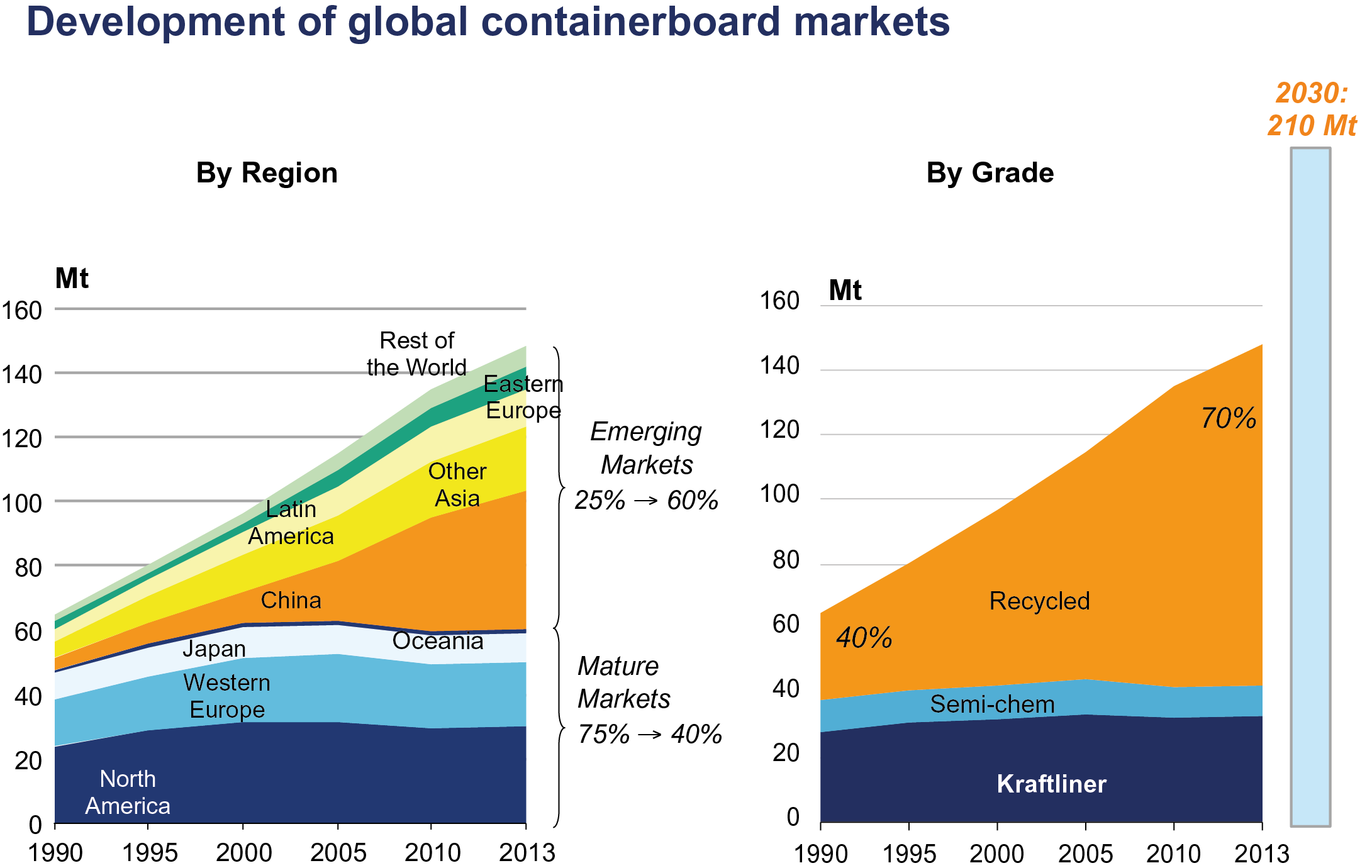

In general, the growth of the world economy, industrial production and merchandise trade are the main demand drivers for containerboards and corrugated board packaging. The current global market is some 150 million tonnes, which is two-and-a-half times the level of 1990. Two drastic changes have taken place during this time: the share of emerging markets has grown from 25 to 60 per cent, with most of the growth occurring in China and other Asian Pacific countries. Today, over half of global consumption resides in the above regions.

The other remarkable change is the boom in recovered fibre-based linerboards and mediums, which now represent 70 per cent of demand, compared to only 40 per cent in 1990. It should be noted, however, that there are significant differences between markets – North America is dominated by kraftliner output and use, while in China only some 10 per cent of containerboard consumption is virgin fibre-based grades. These consumption patterns come directly from corrugated end-use – food is the main end-use in most regions. The exception is in China, where containers are used mainly for packing consumer durables and industrial products (figure 3).

The role of corrugated board as packaging material has changed quite significantly during the past ten to fifteen years. Earlier consumers ran into corrugated only when unpacking often with difficulty, new home electronics. What they saw was mostly heavy, brown square boxes with black printing, used just for protection and transportation. Today, all kind consumer goods from mobile phones to wine are found packed in shiny, colourful cases, which have no resembles with those brown boxes. All carefully designed not only for protection but for attracting consumers and thus functioning as an essential part of sales strategy and product positioning.

Changes expected in the future

An important driver for use of containerboard and corrugated containers has been – and this is expected to continue in the future – its transformation from transport packaging into carefully designed consumer or retail-ready packages with a shiny white surface and high-quality printing. This development is partially driven by the increasing requirements of retail, consumers and brand owners. The corrugated and containerboard industry, however, has also been actively promoting itself, pursuing the growth opportunities represented by this market. The forecast is that global demand in this area will increase by an additional 60 million tonnes by 2030. The global consumption would then reach 210 MT/a.

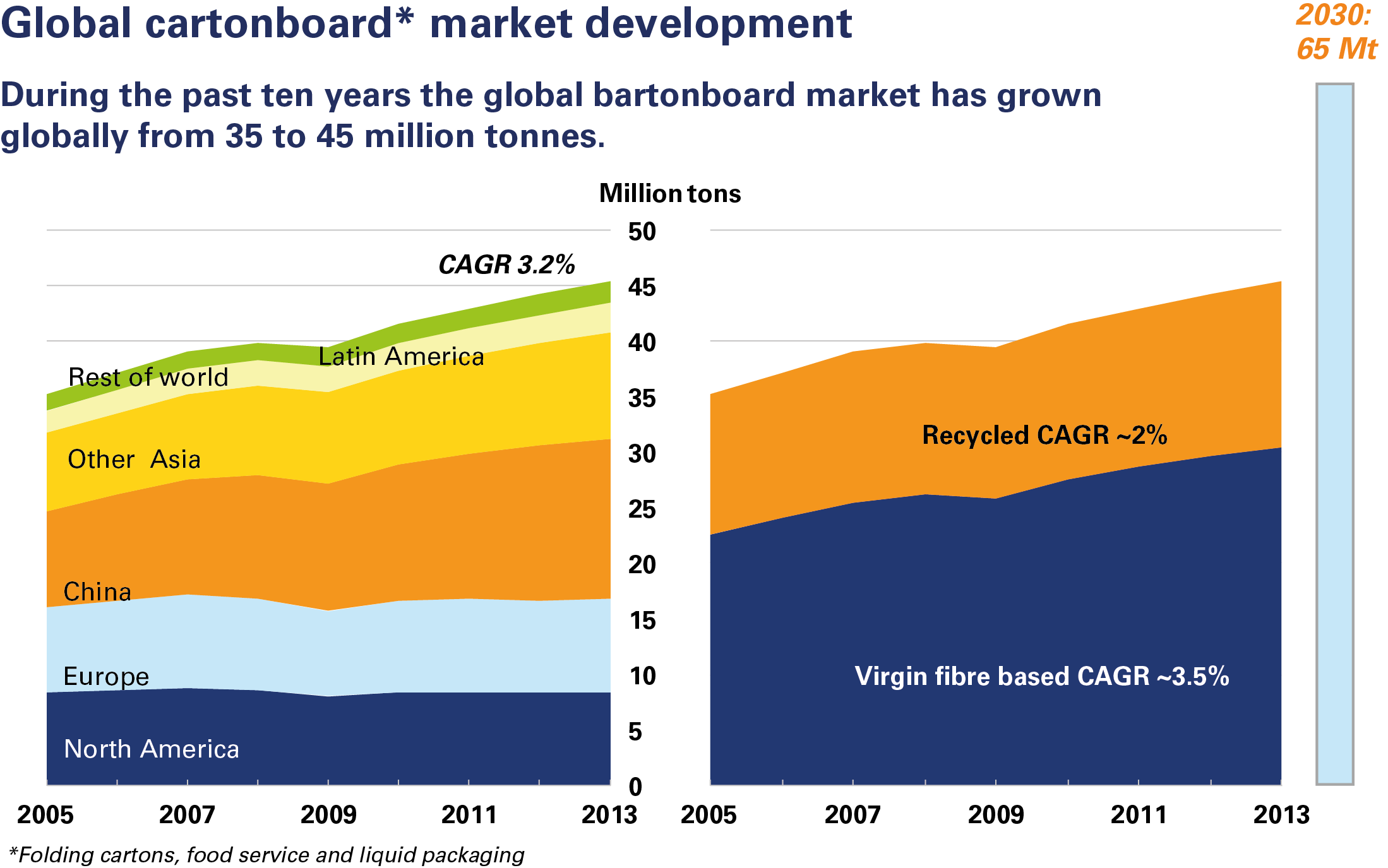

Future looks promising and lucrative opportunities can be found in cartonboards as well. Today, the global market is around 45 million tonnes and is expected to reach 65 million tonnes by 2030. Food packaging — including the fast food segment and liquid packaging — is predominantly driving this demand, particularly in emerging markets.

{kind=link}

However, the more mature markets like Europe and North America are demonstrating fairly good prospects for cartonboards, too. This holds true despite the fact that some of the end-uses like cigarette are declining and substitution to flexible packaging takes place in many products. Due to aging population consumption of pharmaceuticals, health and personal care products continue increasing and position of folding cartons is strong in these segments. Furthermore all food service applications like paper cups, plates and trays are still growing as fast-food chains keep on opening new outlets and eating on-the-go is booming in all the global markets.

All in all the market looks rather good for the fibre based materials; the demand is growing and position of corrugated board, cartonboard and packaging paper solutions is strong and established in many end-use segments. However, one should not forget about the competition. Plastics industry is very innovative and has compelling solutions to offer to the global brand owners. Furthermore packaging industry is becoming increasingly global as the brand owners expand their operations and purchase the regional companies and brands. Serving these companies requires close relationships and a seamlessly functioning supply chain. Fibre based packaging companies is also facing an intense competition within its own industry due to capacity build-up especially in Asia. In China close to 20 MT of new machines have come on stream during the past 15 years leading to the situation where supply and demand are unbalanced.

In order to succeed in this rapidly changing environment and tightening competition the containerboard and cartonboard producers and converters need to pay more and more attention to their R&D, make sure that they talk to the packaging decision makers and have good on-going conversation with the brand owners and at the same time keep their eye on production efficiency and supply chain management. In taking advantage of the existing knowledge, asset base and the hardworking mind-set of this industry has traditionally everything is, however, possible.